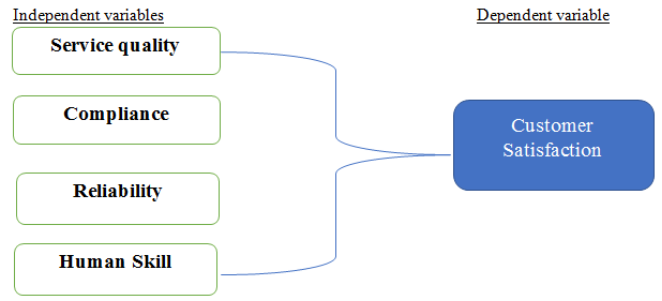

This study examines the impact of digitalization on customer satisfaction in Islamic banking in Ethiopia, focusing on central and eastern regions. A sample of 400 participants was surveyed, with 361 valid responses, using a five-point Likert scale. Data analysis, including explanatory factor analysis and regression, was conducted using SPSS 25 and Amos 23. The results indicate that compliance, reliability, service quality, and human skills significantly and positively influence customer satisfaction with digital Islamic banking. The study's limitations include its focus on a single country, which may limit generalizability to other contexts. Future research could explore cross-cultural differences, longitudinal studies, and qualitative methods to gain deeper insights into customer satisfaction in Islamic banking, especially about technology and global crises like cybersecurity concerns, pandemics, and economic instability. The study suggests that Ethiopian Islamic banks can enhance trust and satisfaction by prioritizing Sharia compliance, investing in staff training, transparent communication, and reliable technology. Customers should support institutions that align with their religious values, fostering long-term relationships. This research addresses a critical gap in understanding customer satisfaction with digital banking services, particularly in global crises such as cybersecurity issues, pandemics, and economic instability. It focuses on how customers of full-fledged Islamic banks perceive and evaluate digital services, the impact of cybersecurity on trust and satisfaction, and the influence of cultural and religious values. Moreover, to the researchers' best knowledge, it is the first study in the country to examine this topic in Islamic banks.

| Published in | International Journal of Finance and Banking Research (Volume 11, Issue 2) |

| DOI | 10.11648/j.ijfbr.20251102.11 |

| Page(s) | 23-36 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Digital Banking, Islamic Banks, Service Quality, Customer Satisfaction

Constructs | İtems |

|---|---|

Customer satisfaction | 3 |

Service quality | 3 |

Compliance | 3 |

Reliability | 4 |

Human Skill | 5 |

Description | frequency | Percentage | |

|---|---|---|---|

Gender | male | 263 | 72.8 |

female | 98 | 28.2 | |

Age | below 25 | 132 | 36.6 |

25 - 35 | 120 | 33.2 | |

36 - 45 | 82 | 22.7 | |

above 45 | 27 | 7.5 | |

Education | High school and bleow | 62 | 17.2 |

diploma | 49 | 13.6 | |

Bachelor | 187 | 51.8 | |

Masters | 49 | 13.6 | |

PhD | 14 | 3.8 | |

Occupation | student | 52 | 22.8 |

civil servant | 191 | 22.5 | |

business employee | 74 | 26.2 | |

Enteprenuer | 44 | 28.5 | |

Experience in using digital banking | 1 - 3 | 198 | 54.8 |

4 - 6 | 108 | 29.9 | |

7 - 9 | 42 | 11.6 | |

Above 10 | 13 | 3.7 | |

How often you use Digital banking products | Daily | 206 | 57.1 |

Weekly | 114 | 31.6 | |

Monthly | 41 | 11.3 | |

Yearly | 0 | 0.0 |

KMO and Bartlett's Test | ||

|---|---|---|

Kaiser-Meyer-Olkin Measure of Sampling Adequacy. | .782 | |

Bartlett's Test of Sphericity | Approx. Chi-Square | 7118.884 |

Df | 171 | |

Sig. | .000 | |

Component | ||||||

|---|---|---|---|---|---|---|

Factor | item | 1 | 2 | 3 | 4 | 5 |

Human Skill | Hskill1 | 0.905 | ||||

Hskill2 | 0.899 | |||||

Hskill5 | 0.895 | |||||

Hskill3 | 0.887 | |||||

Hskill4 | 0.878 | |||||

Service Quality | Serqua4 | 0.951 | ||||

Serqua1 | 0.903 | |||||

Serqua3 | 0.890 | |||||

Reliability | Rel1 | 0.842 | ||||

Rel4 | 0.830 | |||||

Rel3 | 0.830 | |||||

Rel2 | 0.826 | |||||

Compliance | Comp2 | 0.925 | ||||

Comp1 | 0.890 | |||||

Comp3 | 0.884 | |||||

Satisfaction | Sat1 | 0.902 | ||||

Sat2 | 0.867 | |||||

Sat3 | 0.825 | |||||

Variance explained (%) | 32.376 | 14.465 | 18.232 | 10.41 | 7.508 | |

Total variance explained (%) | 82.992 | |||||

Cronbach’s Alpha | 0.854 | |||||

KMO | 0.782 | |||||

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization. a. Rotation converged in 6 iterations. | ||||||

Cronbach’s Alpha | CR | AVE | MSV | ASV | Satis | Hskill | Serqua | Rel | Compl | |

|---|---|---|---|---|---|---|---|---|---|---|

Satis | 0.837 | 0.845 | 0.648 | 0.025 | 0.013 | 0.805 | ||||

Hskill | 0.963 | 0.964 | 0.841 | 0.417 | 0.108 | -0.026 | 0.917 | |||

Serqua | 0.912 | 0.913 | 0.777 | 0.011 | 0.005 | 0.104 | -0.081 | 0.882 | ||

Rel | 0.912 | 0.913 | 0.723 | 0.417 | 0.109 | -0.125 | 0.646 | -0.024 | 0.850 | |

Compl | 0.887 | 0.889 | 0.729 | 0.025 | 0.009 | 0.157 | 0.084 | -0.040 | 0.038 | 0.854 |

Model Fit Indexes | Recommended Limits | Obtained actual result |

|---|---|---|

CMIN (df) | <5 | 213.749/123= 1.738 |

SRMR | <0.05 | 0.036 |

GFI | ≥90 | 0.936 |

AGFI | ≥90 | 0.911 |

NFI | ≥90 | 0.963 |

RFI | ≥90 | 0.954 |

IFI | ≥90 | 0.984 |

TLI | ≥90 | 0.98 |

CFI | ≥90 | 0.984 |

RMSEA | <0.05 | 0.045 |

Estimate | S.E. | C.R. | P | Decision | |||

|---|---|---|---|---|---|---|---|

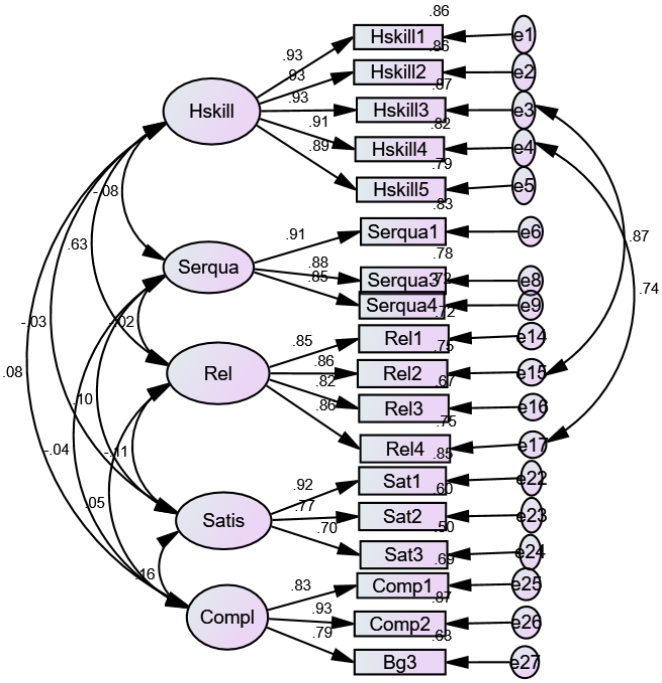

Satis | <--- | Compl | .181 | .052 | 3.468 | *** | Accepted |

Satis | <--- | Rel | .134 | .042 | 3.163 | .002 | Accepted |

Satis | <--- | Serqua | .116 | .047 | 2.453 | .014 | Accepted |

Satis | <--- | Hskill | .126 | .031 | 1.671 | .035 | Accepted |

| [1] | Ab. Aziz, M. R., Jali, M. Z., Mohd Noor, M. N., Sulaiman, S., Harun, M. S., & Mustafar, M. Z. I. (2023). Islamic Digital Banking Based on Maqasid Al-Shariah for Financial Inclusion. I-IECONS e-Proceedings, 289–306. |

| [2] | Abdul Rehman, A. (2012). Customer satisfaction and service quality in Islamic banking: A comparative study in Pakistan, United Arab Emirates and United Kingdom. Qualitative Research in Financial Markets, 4(2–3), 165–175. |

| [3] | Aggarwal, B., Kapoor, D., & Goel, P. (2024). E- service quality and customer satisfaction: A bibliometric retrospective and future research agenda. Environment and Social Psychology, 9(8), 1–14. |

| [4] | Ahmed, R. R., Streimikiene, D., Channar, Z. A., Soomro, R. H., & Streimikis, J. (2021). E-Banking Customer Satisfaction and Loyalty: Evidence from Serial Mediation through Modified E-S-QUAL Model and Second-Order PLS-SEM. Engineering Economics, 32(5), 407–421. |

| [5] | Ahmed, R. R., Vveinhardt, J., Štreimikienė, D., Ashraf, M., & Channar, Z. A. (2017). Modified SERVQUAL model and effects of customer attitude and technology on customer satisfaction in banking industry: mediation, moderation and conditional process analysis. Journal of Business Economics and Management, 18(5), 974–1004. |

| [6] | Aisyah, M. (2018). Islamic Bank Service Quality and Its Impact on Indonesian Customers’ Satisfaction and Loyalty. Al-Iqtishad: Jurnal Ilmu Ekonomi Syariah, 10(2), 367–388. |

| [7] | Akhtar, M. N., Hunjra, A. I., Akbar, S. W., Kashif-Ur-Rehman, & Niazi, G. S. K. (2011). Relationship between customer satisfaction and service quality of Islamic banks. World Applied Sciences Journal, 13(3), 453–459. |

| [8] | Al-Tamimi, H. A. H., & Al-Amiri, A. (2003). Analysing service quality in the UAE Islamic banks. Journal of Financial Services Marketing, 8(2), 119–132. |

| [9] | Alarifi, A. A., & Husain, K. S. (2023). The influence of Internet banking services quality on e-customers’ satisfaction of Saudi banks: comparison study before and during COVID-19. International Journal of Quality and Reliability Management, 40(2), 496–516. |

| [10] | Alfarizi, M. (2023). Interaction of Customer Satisfaction and Retention of Digital Services: PLS Evidence From Indonesian Sharia Banking. International Journal of Islamic Economics and Finance (IJIEF), 6(1), 151–180. |

| [11] | Alfatlawi, N. A. M. A. & H. A. K. (2023). The impact of Digital Technologies on Customer Satisfaction – Opportunities and Challenges. Journal of Current Researches on Business and Economics, 13, 69–77. |

| [12] | Aliya, L., Yetty, F., & Nugraheni, S. (2021). The Effect of The Digitalization of Banking Services on Customer Satisfaction at BCA Syariah KCP Kranji. Journal of Islamic Economics and Social Science (JIESS), 2(2), 114. |

| [13] | Amin, H., Rahim Abdul Rahman, A., Laison Sondoh, S., & Magdalene Chooi Hwa, A. (2011a). Determinants of customers’ intention to use Islamic personal financing. Journal of Islamic Accounting and Business Research, 2(1), 22–42. |

| [14] | Anouze, A. L. M., Alamro, A. S., & Awwad, A. S. (2019). Customer satisfaction and its measurement in Islamic banking sector: a revisit and update. Journal of Islamic Marketing, 10(2), 565–588. |

| [15] | Belwal, R., & Al Maqbali, A. (2019). A study of customers’ perception of Islamic banking in Oman. Journal of Islamic Marketing, 10(1), 150–167. |

| [16] | Berakon, I., Aji, H. M., & Hafizi, M. R. (2022). Impact of digital Sharia banking systems on cash-waqf among Indonesian Muslim youth. Journal of Islamic Marketing, 13(7), 1551–1573. |

| [17] | Beyene, E. (2020). Adoption and Challenges of Mobile Banking Systems in Ethiopia: The Case of Cooperative Bank of Oromiya. The African Conference on Information Systems and Technology, 2008. |

| [18] | Bouafi, S. (2020). The Effects of Digital Banking on Customer Experience, Customer Satisfaction, and Customer Loyalty in Morocco. September, 10–11. |

| [19] | Chakiso, C. B. (2019). Factors affecting Attitudes towards Adoption of Mobile Banking: Users and Non-Users Perspectives. EMAJ: Emerging Markets Journal, 9(1), 54–62. |

| [20] | Cheriyah, Y., Sulistyowati, W., Cornelia, A., & Viverita, V. (2013). Factors Affecting Customers’ Satisfaction and Perception: Case Study of Islamic Banks’Service Quality. ASEAN Marketing Journal, 2(1). |

| [21] | Cherni, S., & Ben Amar, A. (2024). Does digitalization affect shariah supervisory board efficiency? Evidence from Islamic banks. Journal of Islamic Accounting and Business Research. |

| [22] | Costello, A. M., & Osborne, J. A. (2005). Best practices in exploratory factor analysis: Four recommendations for getting the most from your analysis. Practical Assessment, Research, and Evaluation, 10(1), 1–9. |

| [23] | Dandena, S., Abera, T., & Mengesha, T. (2020). Factors affecting the adoption of mobile banking: The case of United Bank Addis Ababa city customers. Journal of Process Management. New Technologies, 8(1), 30–37. |

| [24] | De Bruin, L., Roberts-Lombard, M., & De Meyer-Heydenrych, C. (2021). Internal marketing, service quality and perceived customer satisfaction: An Islamic banking perspective. Journal of Islamic Marketing, 12(1), 199–224. |

| [25] | Demirel, D. (2022). the Effect of Service Quality on Customer Satisfaction in Digital Age: Customer Satisfaction Based Examination of Digital Crm. Journal of Business Economics and Management, 23(3), 507–531. |

| [26] | Dinç, Y., Nagayev, R., & Jahangir, R. (2021). Analysis of Europe’s First Fully-Fledged Islamic Digital Bank in the Arena of New Age Banking. Journal of Islamic Economics, 2(2), 35–53. |

| [27] | Etim, A. S., & Salem, W. (2014). Mobile banking and mobile money adoption for financial inclusion. Research in Business and Economics Journal, 9, 1–13. |

| [28] | Fadayo, O. M. (2018). An Examination of E-Banking Fraud Prevention and An Examination of E-Banking Fraud Prevention and Detection in Nigerian Banks. De Montfort University. |

| [29] | Fadila, Saputra, A., & Etika, C. (2024). Integration of Digital-based Banking Services on Customer Satisfaction (Study of Indonesian Islamic Banks). KnE Social Sciences, 2024, 626–644. |

| [30] | Falk, R. and Miller, N. (1992), APrimer for SoftModeling, The University of Akron, Akron, OH |

| [31] | Guadagnoli, E., & Velicer, W. F. (1988). Relation of sample size to the stability of component patterns. Psychological Bulletin, 103(2), 265–275. |

| [32] | Hadid, K. I., Soon, N. K., & Amreeghah, A. A. E. (2020). The Effect of Digital Banking Service Quality on Customer Satisfaction: A Case Study on the Malaysian Banks. Asian Journal of Applied Science and Technology, 04(01), 06–29. |

| [33] | Hair J, R, A., Babin B, & Black W. (2014). Multivariate Data Analysis.pdf. In Australia : Cengage: Vol. 7 edition (p. 758). |

| [34] | Haque, A., Osman, J., & Ismail, A. Z. H. (2009). Factor influences selection of Islamic banking: A study on Malaysian customer preferences. American Journal of Applied Sciences, 6(5), 922–928. |

| [35] | Hays, W. L. (1983). Review of Using Multivariate Statistics. In Contemporary Psychology: A Journal of Reviews (Vol. 28, Issue 8). |

| [36] | Janahi, M. A., & Al Mubarak, M. M. S. (2017). The impact of customer service quality on customer satisfaction in Islamic banking. Journal of Islamic Marketing, 8(4), 595–604. |

| [37] | Jawaid, S. T., Siddiqui, A. H., Kanwal, R., & Fatima, H. (2023). Islamic banking and customer satisfaction in Pakistan: evidence from internal and external customers. Journal of Islamic Marketing, 14(2), 435–464. |

| [38] | Kaakeh, A., Hassan, M. K., & Van Hemmen Almazor, S. F. (2019). Factors affecting customers’ attitude towards Islamic banking in UAE. International Journal of Emerging Markets, 14(4), 668–688. |

| [39] | Kamiyama, H., & Kashiwagi, K. (2019). Factors affecting customers’ continued intentions to use Islamic banks. Journal of Financial Services Marketing, 24(3–4), 59–68. |

| [40] | Kline, P. (1994). An easy guide to factor analysis. Psychology |

| [41] | Kumar, P., Mokha, A. K., & Pattnaik, S. C. (2022). Electronic customer relationship management (E-CRM), customer experience and customer satisfaction: evidence from the banking industry. Benchmarking, 29(2), 551–572. |

| [42] | Lalwani, K., & Lalbeg, V. K. (2022). A Study of Customer Satisfaction Level towards Digital Banking. 2022 International Conference on Interdisciplinary Research in Technology and Management, IRTM 2022 - Proceedings, 03(01), 161–166. |

| [43] | Legass, H. A. &, & Durmuş, M. E. (2024). Factors determining the adoption of mobile banking in Ethiopian Islamic banks : extension of technology acceptance model (TAM). Journal of Islamic Accounting and Business Research. |

| [44] | Loh, H. S., Lee, J. Le, Gu, Y., Chen, H. S., & Tay, H. L. (2024). The effects of digital platforms on customers’ satisfaction in international shipping business. Review of International Business and Strategy, 34(2), 231–244. |

| [45] | Lone, F. A. (2018). Customer satısfactıon ın full-fledged ıslamıc banks and ıslamıc bankıng wındows : Journal of Internet Banking and Commerce, January 2017. |

| [46] |

Lütfi SÜRÜCÜ. (2019). Exploratory Factor Analysis (EFA) in Quantitative Researches and Practical Considerations. Sustainability (Switzerland), 11(1), 1–14.

http://scioteca.caf.com/bitstream/handle/123456789/1091/RED2017-Eng-8ene.pdf?sequence=12&isAllowed=y%0A http://dx.doi.org/10.1016/j.regsciurbeco.2008.06.005%0Ahttps://www.researchgate.net/publication/305320484_SISTEM_PEMBETUNGAN_TERPUSAT_STRATEGI_MELESTARI |

| [47] | Mamun, M. A. A., Rana, M., Islam, M. A., & Mamun, M. A. (2023). Exploring the factors that affecting adoption of mobile banking in Bangladesh. Journal of Global Business Insights, 8(1), 66–79. |

| [48] | Mbama, C. I., & Ezepue, P. O. (2018). Digital banking, customer experience and bank financial performance: UK customers’ perceptions. International Journal of Bank Marketing, 36(2), 230–255. |

| [49] | Mohd Thas Thaker, H., Mohd Thas Thaker, M. A., Khaliq, A., Allah Pitchay, A., & Iqbal Hussain, H. (2022). Behavioural intention and adoption of internet banking among clients’ of Islamic banks in Malaysia: an analysis using UTAUT2. Journal of Islamic Marketing, 13(5), 1171–1197. |

| [50] | Mousavian, S. J., & Abbasi, H. (2021). Factors Influencing Mobile Banking Adoption in Iranian Clients. Jurnal Bisnis Dan Kewirausahaan (Journal of Business and Entrepreneurship), 9(1), 2021. |

| [51] | Muchammad Ichsan, Fadia Fitriyanti, K. R., & Setiorini, A. M. A.-Q. (2024). Digitalization of Islamic Banking in Indonesia: Justification and Compliance to Sharia Principles. Media Hukum, 31(1), 59-77. |

| [52] | Mulazid, A. S., & Fatmawati, F. (2023). Finding Customer Satisfaction and Loyalty Factors in Islamic Bank Digital Users. Maliki Islamic Economics Journal, 3(1), 19–31. |

| [53] | Muluka, K. O., Kidombo, P. H., Munyolo, W., Oteki, E. B., Scholars, P., & Kenyatta, J. (2015). Effect of Digital Banking on Customer Satisfaction: A case of National Bank of Kenya, Bungoma County. International Journal of Recent Research in Commerce Economics and Management (IJRRCEM), 2(4), 6–14. |

| [54] | Mwiya, B., Katai, M., Bwalya, J., Kayekesi, M., Kaonga, S., Kasanda, E., Munyonzwe, C., Kaulungombe, B., Sakala, E., Muyenga, A., & Mwenya, D. (2022). Examining the effects of electronic service quality on online banking customer satisfaction: Evidence from Zambia. Cogent Business and Management, 9(1). |

| [55] | Nagdev, K., Rajesh, A., & Misra, R. (2021). The mediating impact of demonetisation on customer acceptance for IT-enabled banking services. International Journal of Emerging Markets, 16(1), 51–74. |

| [56] | NBE. (2024). FINANCIAL STABILITY REPORT. April. |

| [57] | Olabode, S. O. (2024). An empirical study on the impact of effective digital customer journey management on customer satisfaction in the Nigerian Islamic banking sector. April. |

| [58] | Pakurár, M., Haddad, H., Nagy, J., Popp, J., & Oláh, J. (2019). The service quality dimensions that affect customer satisfaction in the Jordanian banking sector. Sustainability (Switzerland), 11(4), 1–24. |

| [59] | Patel, R., & Patel, N. (2018). Service quality and customer satisfaction : Study of Indian banks using The Effect of Transformational Leadership, Organizational Learning Capabilities and Innovation on Competitive. Service Quality and Customer Satisfaction : Study of Indian Banks usi. International Journal of Economic Research January 2017, 14(January 2017), 200–211. |

| [60] | Preacher, K. J., & MacCallum, R. C. (2002). Exploratory factor analysis in behavior genetics research: Factor recovery with small sample sizes. Behavior Genetics, 32(2), 153–161. |

| [61] | Qatawneh, A. M., & Makhlouf, M. H. (2023). Influence of smart mobile banking services on senior banks’ clients intention to use: moderating role of digital accounting. Global Knowledge, Memory and Communication. |

| [62] | Raza, S. A., Shah, N., & Ali, M. (2019). Acceptance of mobile banking in Islamic banks: evidence from modified UTAUT model. Journal of Islamic Marketing, 10(1), 357–376. |

| [63] | Reta Entele, B. (2019). Mobile Banking Technology in Ethiopia: Adoption and implication for Financial Service Inclusion. Ethiopian Journal of Science and Sustainable Development, 6(2), 2019. |

| [64] | Rezeki, M. R., Majid, M. S. A., & Kassim, S. H. (2023). The effect of e-service quality on e-loyalty of Islamic banking customers: Does e-satisfaction act as mediator? Jurnal Ekonomi & Keuangan Islam, 9(2), 228–245. |

| [65] | Riza, A. F., & Wijayanti, D. M. (2024). Strengthening a sustainable Islamic financial industry through digital banking. Journal of Islamic Marketing. |

| [66] | Saeed, R., Iqbal, A., Nawaz Lodhi, R., Sami, A., Riaz, A., & Munir, M. (2014). Impact of Service Quality on Customer Loyalty in Islamic Banking Sector of Pakistan: A Mediating Role of Customer Satisfaction. J. Basic. Appl. Sci. Res, 4(2), 135–143. |

| [67] | Saqib, L., Farooq, M. A., & Zafar, A. M. (2016). Customer perception regarding Sharī‘ah compliance of Islamic banking sector of Pakistan. Journal of Islamic Accounting and Business Research, 7(4), 282–303. |

| [68] | Shabani, L., Behluli, A., Qerimi, F., Pula, F., & Dalloshi, P. (2022). The Effect of Digitalization on the Quality of Service and Customer Loyalty. Emerging Science Journal, 6(6), 1274–1289. |

| [69] | Sharif Bashir, M. (2012). Analysis of Customer Satisfaction with the Islamic Banking Sector: Case of Brunei Darussalam. Asian Journal of Business and Management Sciences, 2(10), 38–50. |

| [70] | Sidaoui, M., Ben Bouheni, F., Arslankhuyag, Z., & Mian, S. (2022). Fintech and Islamic banking growth: new evidence. Journal of Risk Finance, 23(5), 535–557. |

| [71] | Sutikno, S., Nursaman, N., & Muliyat, M. (2022). The Role Of Digital Banking In Taking The Opportunities And Challenges Of Sharia Banks In The Digital Era. Journal of Management Science (JMAS), 5(1), 27–30. |

| [72] | Taap, M. A., Chong, S. C., Kumar, M., & Fong, T. K. (2011). Measuring service quality of conventional and Islamic banks: A comparative analysis. International Journal of Quality and Reliability Management, 28(8), 822–840. |

| [73] | Torres Fragoso, J., & Luna Espinoza, I. (2017). Evaluación de la percepción de la calidad de los servicios bancarios mediante el modelo SERVPERF. Contaduria y Administracion, 62(4), 1294–1316. |

| [74] | Yussaivi, A., Suhartanto, D., & Syarief, M. E. (2020). An Analysis of the Determining Factors of Mobile Banking Adoption in Islamic Banks. IOP Conference Series: Materials Science and Engineering, 879(1), 1–8. |

| [75] | Yusuf, M., Adinugraha, H. H., & Abadi, M. T. (2022). the Effect of Marketing Mix, Self-Service Technology, and Digital Banking on Customer Satisfaction At Indonesian Sharia Bank of Pekalongan Pemuda. Journal of Management and Islamic Finance, 2(1), 1–11. |

| [76] | Zeitun, R., & Anam, O. A. (2024). Do product offering and service quality affect customer satisfaction in Islamic and conventional banks? Evidence from an oil-based economy. Journal of Islamic Marketing. |

| [77] | Ziaulhaq Mamun, M., & Huque Khan, R. (2014). Customers’ Satisfaction of Islamic Banking and Conventional Banking in Bangladesh: A Comparative Study. Journal of Business Studies, XXXV(1). |

| [78] | Zouari, G., & Abdelhedi, M. (2021a). Customer satisfaction in the digital era: evidence from Islamic banking. Journal of Innovation and Entrepreneurship, 10(1). |

APA Style

Legass, H. A., Mekonnen, D. C., Yusuf, J. M. (2025). Islamic Banking Customers Satisfaction in the Digital Banking: Evidence from Ethiopia: A SEM Approach. International Journal of Finance and Banking Research, 11(2), 23-36. https://doi.org/10.11648/j.ijfbr.20251102.11

ACS Style

Legass, H. A.; Mekonnen, D. C.; Yusuf, J. M. Islamic Banking Customers Satisfaction in the Digital Banking: Evidence from Ethiopia: A SEM Approach. Int. J. Finance Bank. Res. 2025, 11(2), 23-36. doi: 10.11648/j.ijfbr.20251102.11

AMA Style

Legass HA, Mekonnen DC, Yusuf JM. Islamic Banking Customers Satisfaction in the Digital Banking: Evidence from Ethiopia: A SEM Approach. Int J Finance Bank Res. 2025;11(2):23-36. doi: 10.11648/j.ijfbr.20251102.11

@article{10.11648/j.ijfbr.20251102.11,

author = {Habtamu Alebachew Legass and Dawud Chane Mekonnen and Jundi Mohammed Yusuf},

title = {Islamic Banking Customers Satisfaction in the Digital Banking: Evidence from Ethiopia: A SEM Approach

},

journal = {International Journal of Finance and Banking Research},

volume = {11},

number = {2},

pages = {23-36},

doi = {10.11648/j.ijfbr.20251102.11},

url = {https://doi.org/10.11648/j.ijfbr.20251102.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijfbr.20251102.11},

abstract = {This study examines the impact of digitalization on customer satisfaction in Islamic banking in Ethiopia, focusing on central and eastern regions. A sample of 400 participants was surveyed, with 361 valid responses, using a five-point Likert scale. Data analysis, including explanatory factor analysis and regression, was conducted using SPSS 25 and Amos 23. The results indicate that compliance, reliability, service quality, and human skills significantly and positively influence customer satisfaction with digital Islamic banking. The study's limitations include its focus on a single country, which may limit generalizability to other contexts. Future research could explore cross-cultural differences, longitudinal studies, and qualitative methods to gain deeper insights into customer satisfaction in Islamic banking, especially about technology and global crises like cybersecurity concerns, pandemics, and economic instability. The study suggests that Ethiopian Islamic banks can enhance trust and satisfaction by prioritizing Sharia compliance, investing in staff training, transparent communication, and reliable technology. Customers should support institutions that align with their religious values, fostering long-term relationships. This research addresses a critical gap in understanding customer satisfaction with digital banking services, particularly in global crises such as cybersecurity issues, pandemics, and economic instability. It focuses on how customers of full-fledged Islamic banks perceive and evaluate digital services, the impact of cybersecurity on trust and satisfaction, and the influence of cultural and religious values. Moreover, to the researchers' best knowledge, it is the first study in the country to examine this topic in Islamic banks.

},

year = {2025}

}

TY - JOUR T1 - Islamic Banking Customers Satisfaction in the Digital Banking: Evidence from Ethiopia: A SEM Approach AU - Habtamu Alebachew Legass AU - Dawud Chane Mekonnen AU - Jundi Mohammed Yusuf Y1 - 2025/03/21 PY - 2025 N1 - https://doi.org/10.11648/j.ijfbr.20251102.11 DO - 10.11648/j.ijfbr.20251102.11 T2 - International Journal of Finance and Banking Research JF - International Journal of Finance and Banking Research JO - International Journal of Finance and Banking Research SP - 23 EP - 36 PB - Science Publishing Group SN - 2472-2278 UR - https://doi.org/10.11648/j.ijfbr.20251102.11 AB - This study examines the impact of digitalization on customer satisfaction in Islamic banking in Ethiopia, focusing on central and eastern regions. A sample of 400 participants was surveyed, with 361 valid responses, using a five-point Likert scale. Data analysis, including explanatory factor analysis and regression, was conducted using SPSS 25 and Amos 23. The results indicate that compliance, reliability, service quality, and human skills significantly and positively influence customer satisfaction with digital Islamic banking. The study's limitations include its focus on a single country, which may limit generalizability to other contexts. Future research could explore cross-cultural differences, longitudinal studies, and qualitative methods to gain deeper insights into customer satisfaction in Islamic banking, especially about technology and global crises like cybersecurity concerns, pandemics, and economic instability. The study suggests that Ethiopian Islamic banks can enhance trust and satisfaction by prioritizing Sharia compliance, investing in staff training, transparent communication, and reliable technology. Customers should support institutions that align with their religious values, fostering long-term relationships. This research addresses a critical gap in understanding customer satisfaction with digital banking services, particularly in global crises such as cybersecurity issues, pandemics, and economic instability. It focuses on how customers of full-fledged Islamic banks perceive and evaluate digital services, the impact of cybersecurity on trust and satisfaction, and the influence of cultural and religious values. Moreover, to the researchers' best knowledge, it is the first study in the country to examine this topic in Islamic banks. VL - 11 IS - 2 ER -

Research Center of Islamic Economics and Finance, Sakarya University, Sakarya, Türkiye

Department of Public Administration and Development Management, Dire Dawa University, Dire Dawa, Ethiopia

Department of Accounting and Finance, Dire Dawa University, Dire Dawa, Ethiopia